11 Mar College Savings in 2015

5 Tips for Saving for College in 2015 ThinkAdvisor. https://www.thinkadvisor.com/2015/03/05/5-tips-for-saving-for-college-in-2015

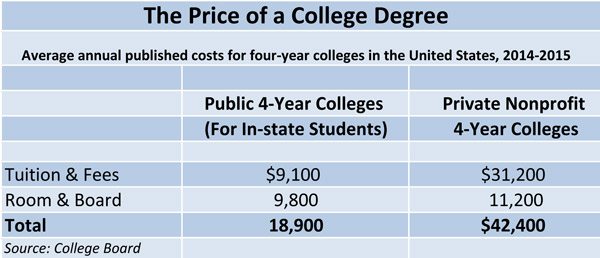

529 plans are one of the best ways to accumulate compounded, untaxed returns, but there are some other solid pathways to college saving. Paying for college is among the most significant expenses many families will ever have, second only to buying a home. According to the College Board, total tuition, fees, room, and board this year average $19,000 for a four-year college for in-state residents and $42,000 for a private nonprofit four-year institution. Multiply those numbers by four—or even more since many don’t graduate in four years—and the costs are minimally $76,000 for a four-year public institution and $168,000 for a private one at current rates. Moreover, those rates are likely to rise in the future.

Given this reality, families must have a college funding plan. Even if students qualify for some financial aid or scholarship, they’re not likely to get a completely free ride—fewer than 0.3% do, says Mark Kantrowitz, Senior Vice President and publisher of Edvisors.com, a website focused on planning and paying for college.

Here are five basics advisors should inform their clients regarding college planning for their children and grandchildren. imperative for families to have a college funding plan. Even if students qualify for some financial aid or scholarship they’re not likely to get a completely free ride—fewer than 0.3% do, says Mark Kantrowitz, Senior VP and publisher of Edvisors.com, a website focused on planning and paying for college.

Here are five basics that advisors should inform their clients regarding college planning for their children and grandchildren.

1. Fund a College Savings Plan Early and Often

“Every dollar you save is a dollar you don’t have to borrow,” says Kantrowiz. “And every $1 you borrow costs $2 by the time you pay back debt.”

Starting early also means saving less in the long run because savings will grow from earnings. “If you start saving sooner than later, about one-third of the fund’s size will come from earnings,” says Kantrowitz, but if you wait until the student is in high school, “less than 10% will.”

What doesn’t come from earnings has to come from contributions.

2. Open a 529 College Savings Account

The 529 College Savings Account is a popular college funding plan that approximately 12 million American families use. Investments in these plans grow tax-deferred, and distributions used to pay college costs are free from federal income taxes. You can open plans outside your state, but first, check if your state’s plan offers full or partial deductions or tax credits for contributions. Thirty-four states plus the District of Columbia do, and six states allow deductions for contributions to out-of-state plans: Pennsylvania, Arizona, Kansas, Maine, Missouri, Montana, and Pennsylvania.

Contribution limits are often above $250,000, but withdrawals can be used only for qualified higher education expenses such as tuition, room and board, mandatory fees, and books.

Most plans have several investment options—usually different mutual funds—but some also include ETFs, Certificates of Deposit, and guaranteed investment options. Starting this year, investors can change portfolios twice a year instead of once.

For more about 529 different plans, check out Savingforcollege.com’s latest rankings: 2014 plan performance rankings Q4.

3. Consider a Prepaid Tuition Plan

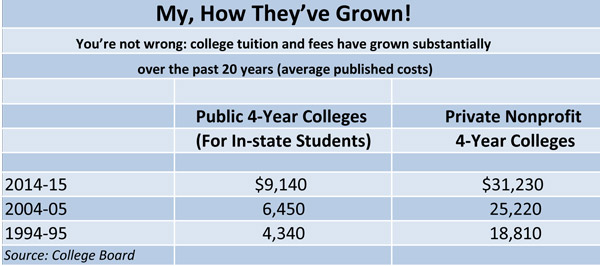

These plans lock in tuition costs at current levels, which can be a significant benefit considering that college costs are rising yearly—usually above the inflation rate. Today, tuition and fees for a private nonprofit four-year college average about $31,000, up 24% from 10 years ago and 66% from 20 years ago, after adjusting for inflation, according to the College Board. The increase is even more dramatic for four-year public institutions because of state funding cuts.

Tuition and fees today average $9,100, up 42% from 10 years ago and more than double the costs 20 years ago after adjusting for inflation.

There are two types of prepaid tuition plans: state plans, which allow state residents to lock in tuition and fees at a state college or university, and the Private College 529 Plan offered by the Tuition Plan Consortium, which covers 270 private institutions, including MIT, Duke, and Syracuse University.

Note these caveats: State plans are subject to changing state economics, so check if that particular state’s full faith and credit back a plan. If your student decides not to attend a public-state institution, the plan can be converted for use at private and out-of-state institutions, but you should know the details before investing.

The Private College 529 Plan is also convertible into a traditional 529 plan if your student doesn’t attend any participating colleges.

4. Understand the Relationship Between College Savings and Financial Aid

Before every academic year, families are required to fill out the dreaded FAFSA (Free Application for Federal Student Aid) to qualify for financial aid. You should do this even if you don’t think your student will qualify. Once the form is completed, it will calculate the Expected Family Contribution (EFC).The higher the EFC, the less financial aid available, if any.

Here’s a quick primer:

- 529 Plans owned by students or their parents are considered assets of the parents, and parents are expected to use 5.64% of those assets to pay for college. Assets in a child’s name, like Coverdell Education Savings Accounts (formerly known as an Education IRA), are assessed at a 20% contribution rate. For example, $10,000 in a 529 plan translates into a $564 contribution, but $10,000 in a Coverdell translates into a $2,000 contribution. Plans owned by a student or by his or her parents are considered assets of the parents, and parents are expected to use 5.64% of those assets to pay for college. Assets in a child’s name like a Coverdell Education Savings Accounts (formerly known as an Education IRA) are assessed at a 20% contribution rate. For example, $10,000 in a 529 plan translates into a $564 contribution but $10,000 in a Coverdell translates into a $2,000 contribution.

- FAFSA does not consider 529 plans owned by a grandparent or a Roth IRA owned by a parent, but it will count distributions from those plans once they’re used to help pay for college. Those contributions will be considered part of the student’s income the following year, and about half will be included in the EFC. With that in mind, these distributions are best used for the last year of college because there won’t be another FAFSA form to complete.

- Kantrowitz suggests a parent’s Roth IRA distribution be used soon after graduation to help a college graduate pay down some debt.

5. Keep Track of Changing Laws and Regs

The Higher Education Act controls most federal student aid programs and is up for reauthorization this year. Senator Lamar Alexander (R-Tenn.), chairman of the Health, Education, Labor and Pensions (HELP) Committee, will lead the process and has already introduced a bill to simplify the FAFSA form, establish just one grant and one loan program for student aid and restore Pell grants.

President Obama’s proposal for a new college ratings system is also pending. His proposal for free community college tuition is not expected to go anywhere.

As an example of how important it is to keep track of changes in federal and state laws and regulations regarding college tuition funding, on Feb. 25, the House of Representatives passed a bill (H.R. 529) with broad bipartisan support (by a vote of 401-20). It would allow students to use 529 distributions to pay for computers, software, and Internet access while in college. A similar bill (S. 335) has been introduced in the Senate and is now before the Senate Finance Committee.

Sorry, the comment form is closed at this time.